Profit and gains from business or profession under Income tax, 2025

May 15, 2026

- Introduction:

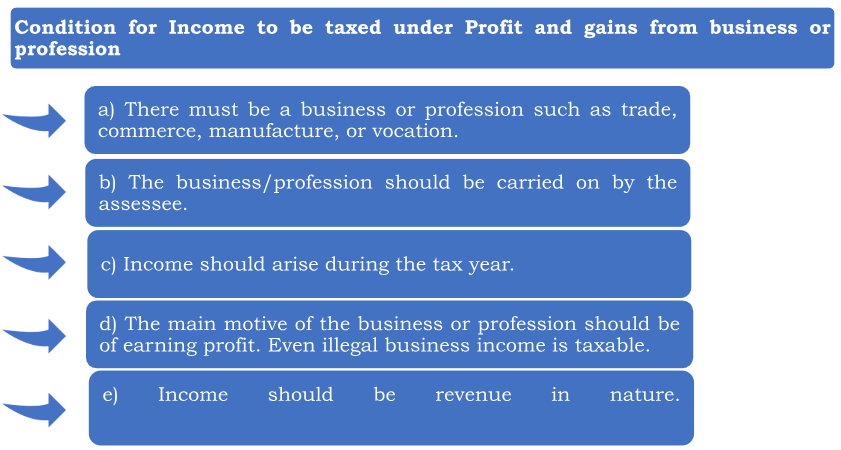

Profit and gains from business or profession is one of the heads of the income under the Income Tax Act, 2025 which deals with the taxation of income earned from carrying on any business or profession during a Tax year.

- Profit and gains from business or profession under charging section:

Section 28 (Income Tax Act 1961) TO Section 26 (Income Tax Act 2025):

Income in the form of profit and gains arising from any business or profession carried on during the tax year, which is chargeable to tax under profit and gains from business or profession head of income.

- The income under 26 shall include:

- The profit and gains of any business or profession carried on by the assessee at any time during the tax year.

- Covers compensation or payment related to business/profession.

Includes amount received for:

- Termination of business contracts

- Modification of agreements

- Managing business affairs

- Any profit on sale of business assets or receipts arising from business operations.

- Any other income which is incidental to or arises from the carrying on of any business or profession.

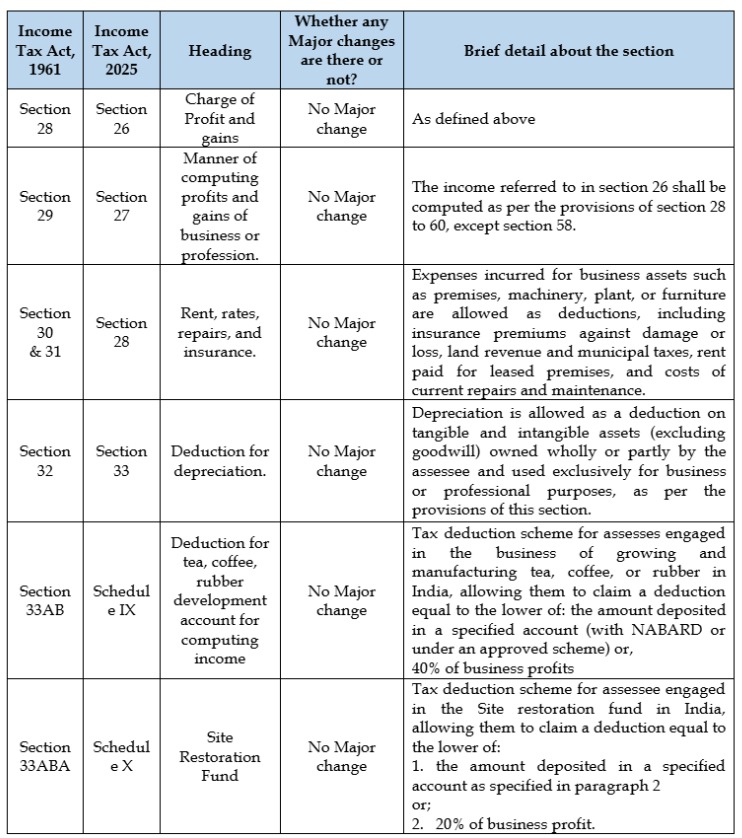

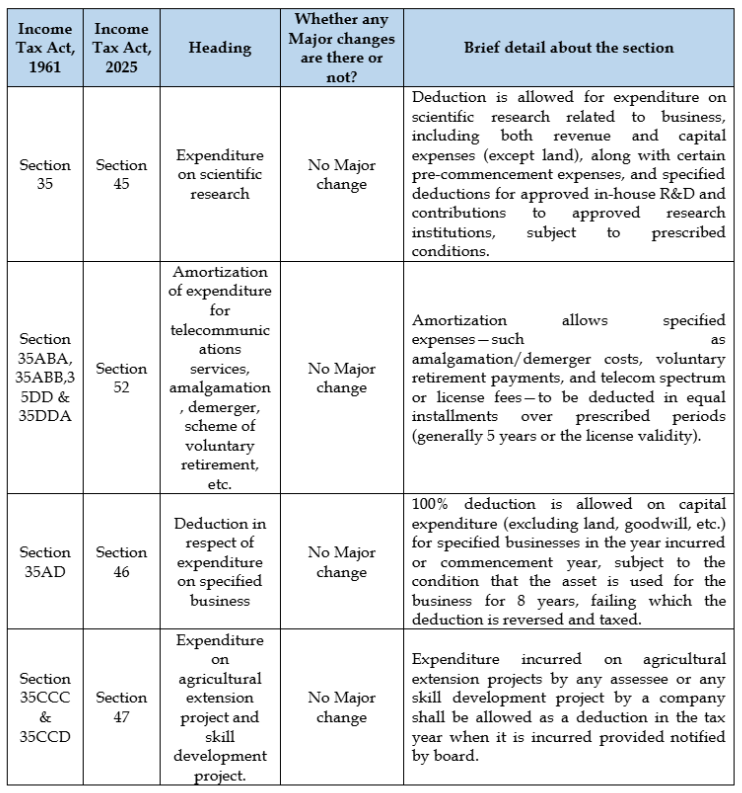

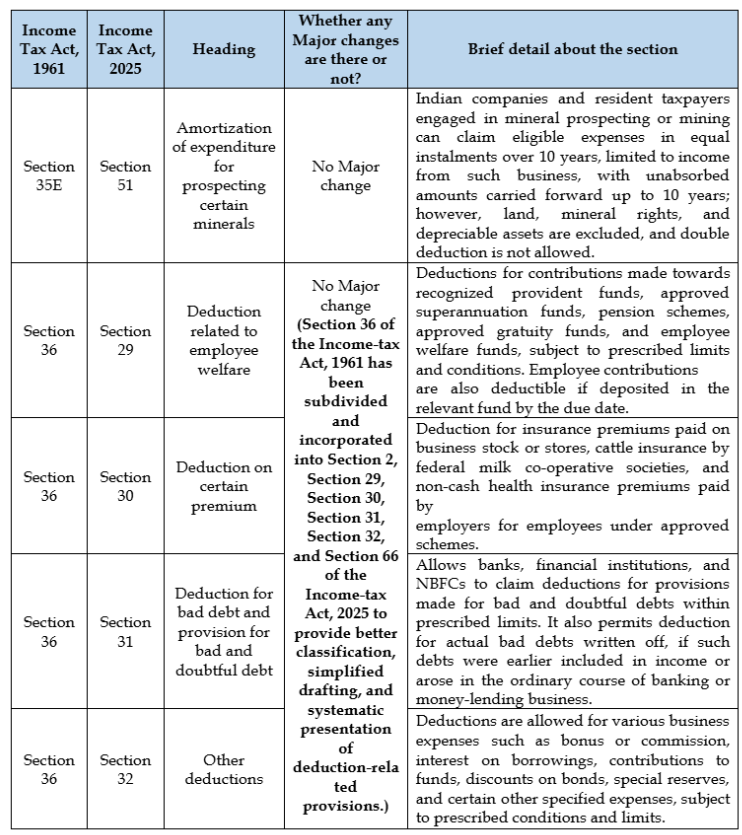

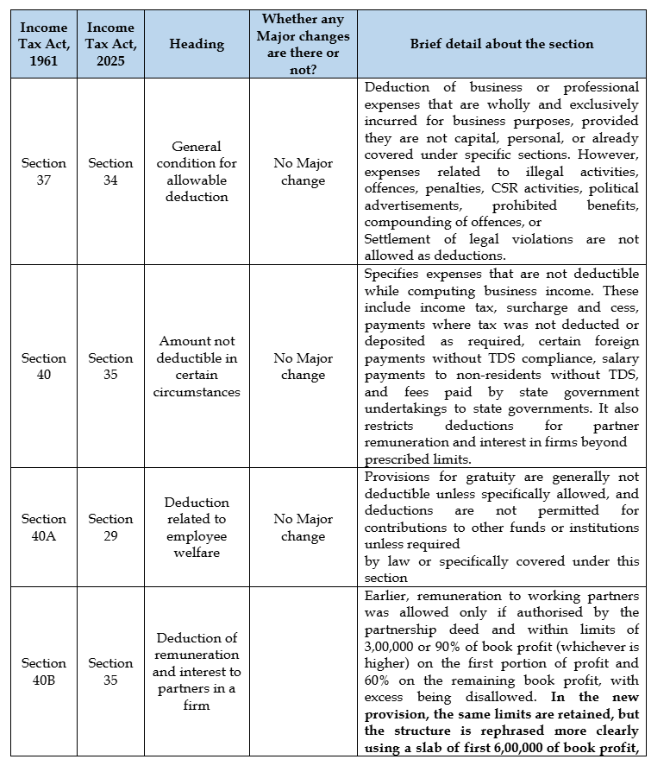

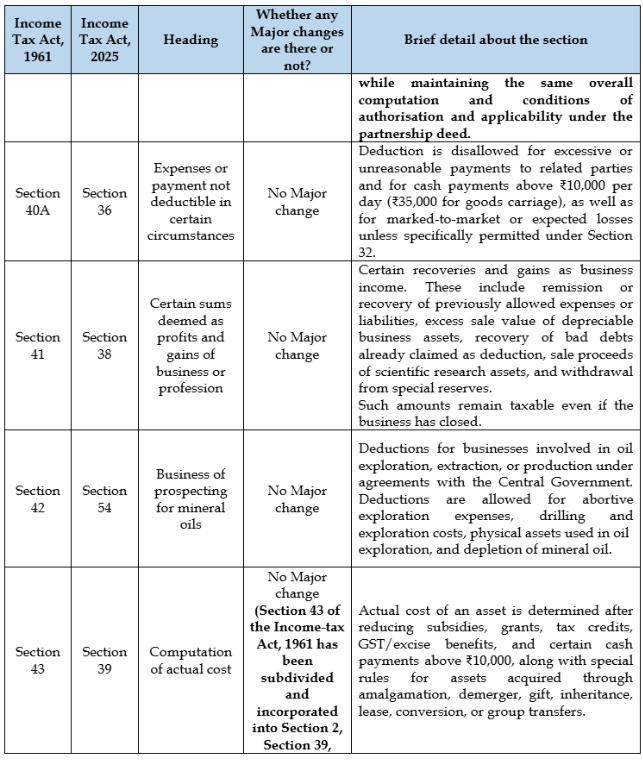

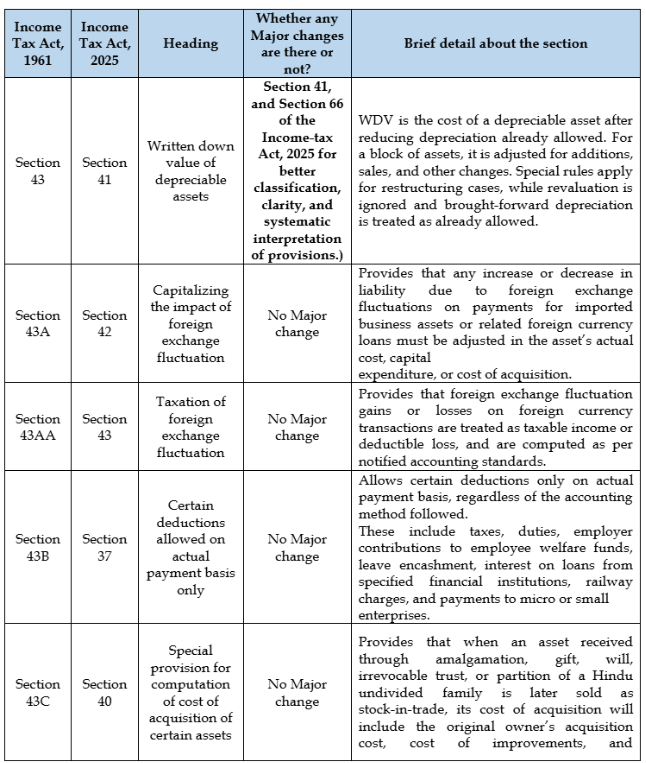

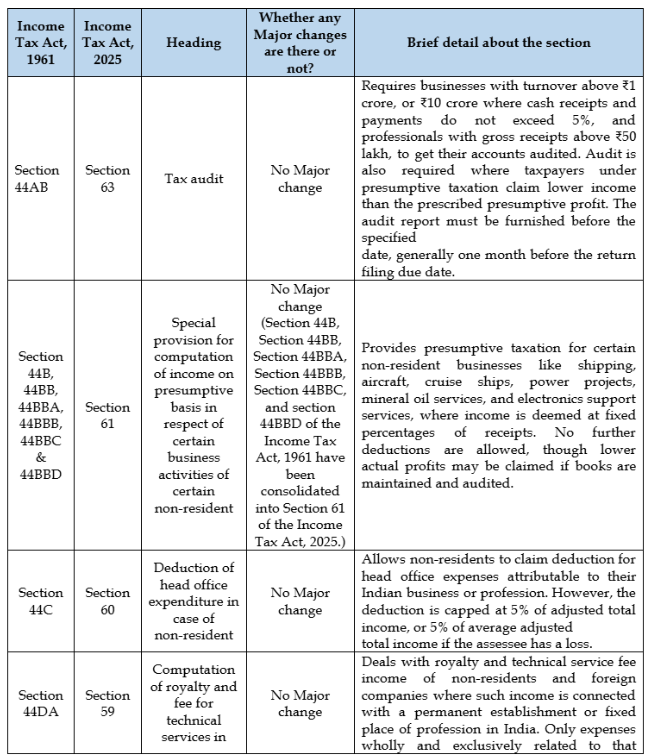

- To facilitate a better understanding of Profit and gains from business and profession, a comparative mapping of the key provision under the Income Tax Act, 1961 and revised provision under the Income Tax Act, 2025 has been provided below. The following table highlights how existing sections has been aligned within the new structure.

- Conclusion:

The provisions relating to Profits and Gains from Business or Profession under the Income Tax Act, 2025 create a comprehensive framework for determining taxable business income. They cover the allowability of business expenses, depreciation, presumptive taxation, maintenance of books, tax audit, treatment of non-residents, and special provisions for sectors such as banking, insurance, shipping, mineral oil, and professional services. The law aims to ensure that only genuine business expenses are deducted, while preventing misuse through restrictions on cash payments, related-party transactions, and non-compliance with tax deduction requirements. Overall, the PGBP provisions promote transparency, proper record-keeping, and fair taxation, while also providing relief and simplified compliance for small businesses, professionals, and specified industries

Authors:

Vishal Kothari

Director | LinkedIn Profile

Nitesh Jha

Manager | LinkedIn Profile

Gaurav Gohil

Associate Consultant |LinkedIn Profile

Anjali Padhariya

Associate Consultant |LinkedIn Profile

.svg)