Old TDS Sections vs Amended TDS Sections under Income Tax Act, 2025

Introduction

Tax Deducted at Source (TDS) is a mechanism of revenue collection by Government under the income tax whereby tax is deducted at the point of generation of income rather than at a later stage. Under this system, the person responsible for making specified payments such as salary, interest, rent, commission, or professional fees is required to deduct a prescribed percentage of tax before making the payment to the recipient. The amount so deducted is then deposited with the government on behalf of the payee.

TDS provisions under the Income Tax Act, 2025 has been amended to improve compliance, widen the tax base and to simplify the process of filing the TDS. This article explains the difference between TDS sections as per Income Tax Act, 1961 and newly enacted Income Tax Act, 2025.

Objectives and Significance of TDS

The primary objective of TDS is to ensure a steady inflow of revenue to the government and to minimize tax evasion by collecting tax at the earliest point of income accrual. It also facilitates better compliance by spreading the tax liability over the financial year, reducing the burden on taxpayers at the time of filing returns. Additionally, TDS creates a transparent reporting system, as the deducted tax is reflected in the taxpayer’s records, enabling accurate tracking and reconciliation of income and taxes

Need for Reorganisation of Existing Provisions

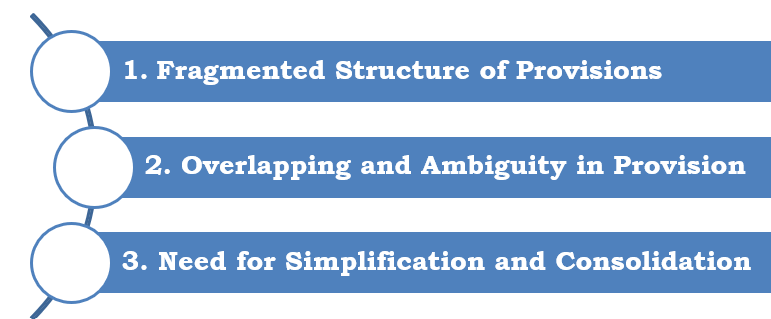

The existing TDS framework under the Income Tax Act, 1961 required amendments due to the following key factors:

1. Fragmented Structure of Provisions

The earlier Income Tax Act, 1961 TDS consisted of multiple standalone sections, each dealing with specific types of transactions. This fragmented structure made interpretation difficult and increased the chances of errors incompliance. A consolidated framework was necessary to simplify application andimprove clarity.

2. Overlapping and Ambiguity in Provisions

Certain transactions were covered under multiple TDS sections, creatingconfusion regarding applicability. This increased the risk of incorrect deduction or duplication. A more streamlined structure was needed to eliminate overlaps and provide clear guidance.

3. Need for Simplification and Consolidation

With increasing compliance requirements, there was a strong need to simplify the TDS framework. Consolidating provisions into a single structured section improves readability and ease of implementation. This also helps businesses manage compliance more efficiently

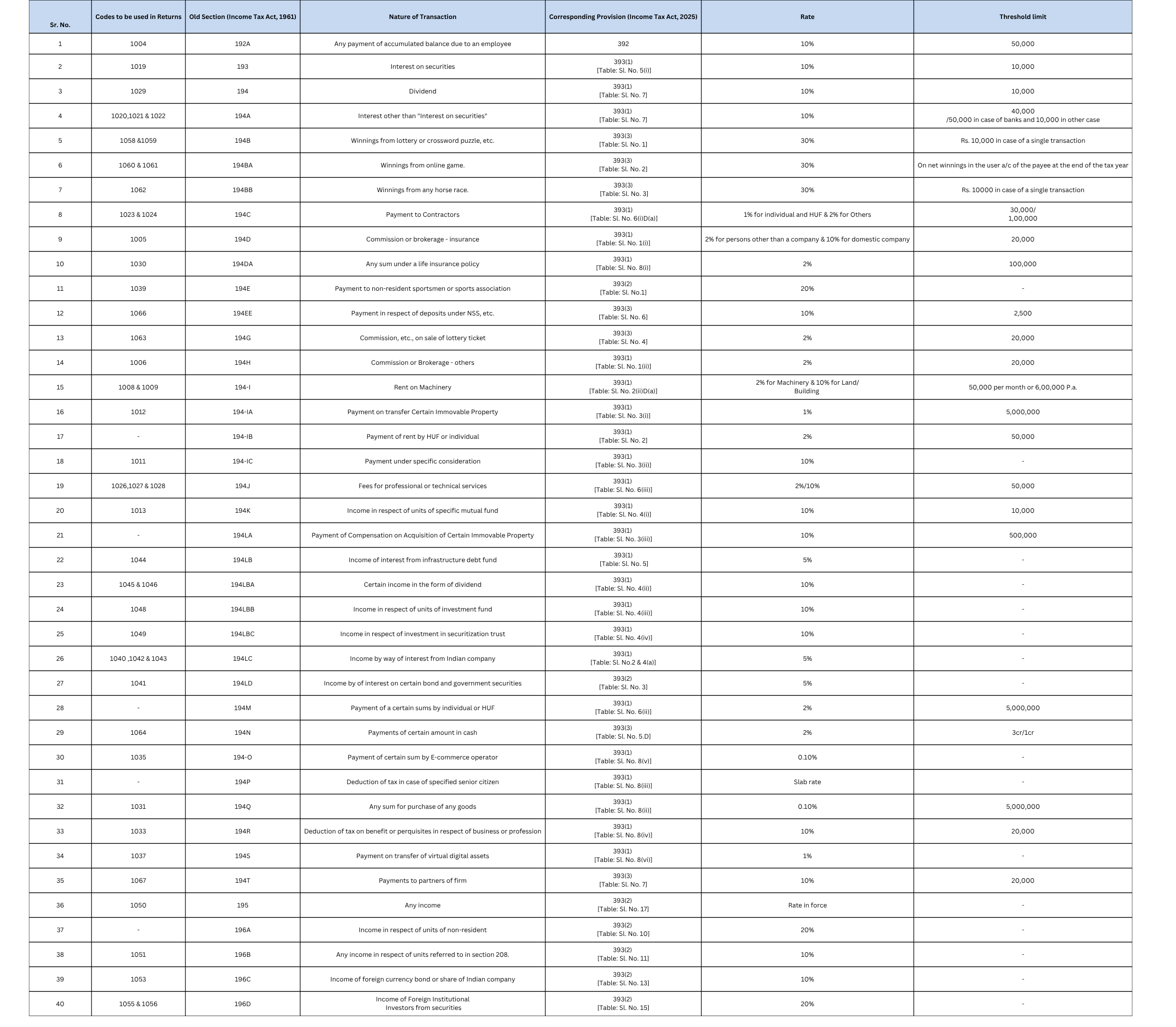

Overview of the TDS Framework in the Newly enacted Income TaxAct, 2025 and Comparative Analysis

The revised TDS framework introduces a significant structural shift by consolidating multiple provisions into aunified system under Section 393. These changes have been proposed as part of the recent Income Tax Act, 2025 with the objective of simplifying and modernising the existing tax structure. This change enhances clarity, improves accessibility, and simplifies the process of identifying applicable provisionsfor various transactions.

To facilitate a better understanding of this transition, a comparative mapping of the key TDS provisions under the Income Tax Act, 1961 and the revised provisions under the Income Tax Act, 2025 hasbeen provided below. The table highlights how existing sections have beenaligned within the new structure, along with key changes in terms of scope,thresholds, and applicability. This comparison enables businesses andprofessionals to easily interpret the impact of the revised provisions andadapt their compliance processes accordingly.

Lower Deduction Certificate

In addition to the standard provisions relating to Tax Deducted atSource, taxpayers also have the option to apply for a lower deduction certificate where the actual tax liability is expected to be lower than the prescribed TDS rates. Under Section 395 of the Income Tax Act, 2025, an application may be made to the tax authorities in the prescribed form forobtaining such a certificate. Under the earlier framework of the Income TaxAct, 1961, such application was made in Form No. 13, whereas under the revised framework it is proposed to be made in Form No. 128, as may be notified. Upon issuance of the certificate, the payer is authorised to deduct tax at are duced rate. This mechanism helps in avoiding excess deduction of tax,improves cash flow for taxpayers, and ensures that tax is deducted moreaccurately in line with the actual liability.

Conclusion

The transition from multiple standalone TDS provisions to a consolidated framework represents a significant step towards simplifying and modernising the tax structure. By bringing various provisions under a unified system, the revised approach enhances clarity, reduces complexity, and improves ease of compliance for businesses and professionals. While the fundamental principles of Tax Deducted at Source remain unchanged, the restructured format aligns the framework with evolving business practices and emerging transaction types, thereby enabling a more efficient, transparent and streamlined tax compliance environment.

Authors:

Vishal Kothari

Partner | LinkedIn Profile |

Nitesh Jha

Manager | LinkedIn Profile |

Gaurav Gohil

Associate Consultant | LinkedIn Profile |

Ayush shah

Associate Consultant | LinkedIn Profile |

For Inquiries:

Email: https://bilimoriamehta.in/blogs/ |

Contact: +91 9320614111|

.svg)