Income from House Property as per the Income Tax Act, 2025:

Introduction:

Income under the head House Property means income earned from owning and letting out a building or the land attached to it through lease payments, rentals or deemed rent, and it is taxed based on its annual value. Earlier, it was governed by Sections 22 to 27 of the Income-tax Act, 1961; however, under the Income-tax Act, 2025, it is now covered under Sections 20 to 25.

The Income-tax Act, 2025, does not introduce any material changes affecting the taxability of income under the head “Income from House Property” vis-à-vis the Income-tax Act, 1961. The provisions relating to chargeability, computation, and admissible deductions continue to remain substantially the same, with the 2025 Act primarily being a restructuring and simplification of the existing law.

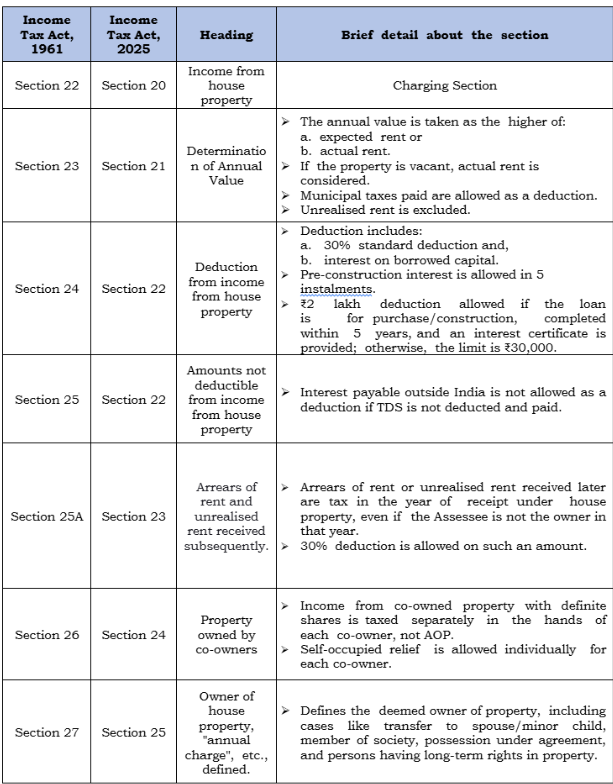

Comparative Analysis of Income under the Head of House Property

Authors:

Vishal Kothari

Director | LinkedIn Profile

Nitesh Jha

Manager | LinkedIn Profile

Rutwick Ruparelia

Manager | LinkedIn Profile

Krisha Chaudhari

Consultant | LinkedIn Profile

Gaurav Gohil

Associate Consultant |LinkedIn Profile

.svg)