Income From Other Sources under the Income Tax Act, 2025

Introduction (Charging Section – 92(1)

Any income which is not specifically taxable under the heads of Salary, House Property, Profits and Gains from Business or Profession (PGBP), or Capital Gains shall be taxable under the head Income from Other Sources.

This head acts as a residuary head of income, meaning it covers incomes that do not fall under any other specific category but are still taxable in nature. The objective of this section is to ensure that no taxable income escapes taxation merely because it does not fit within the other prescribed heads of income.

Table 1: Overview of Sections under the head “Other Sources”

Table 2: Given below are the examples of income that are taxable under the head income from other sources:

Note 1: Section 2(40): Dividend Income

Dividends from shares.

Where the recipient is a resident: Dividend income shall be taxable at the applicable slab rates. A deduction for interest expenditure incurred to earn such income shall be allowed, subject to a maximum of 20% of the total dividend income.

Where the recipient is a non-resident: Dividend income shall be taxable at a special rate of 20%, subject to the provisions of the applicable DTAA (Double Taxation Avoidance Agreement). No deduction for any expenditure shall be allowed against such income.

Table 3: Detailed description of deemed dividend.

Deemed Dividend (Section 2(40)(a) – 2(40)(e))

Following Distribution by a Company to its shareholders is deemed as dividend (to the extent of Accumulated Profits).

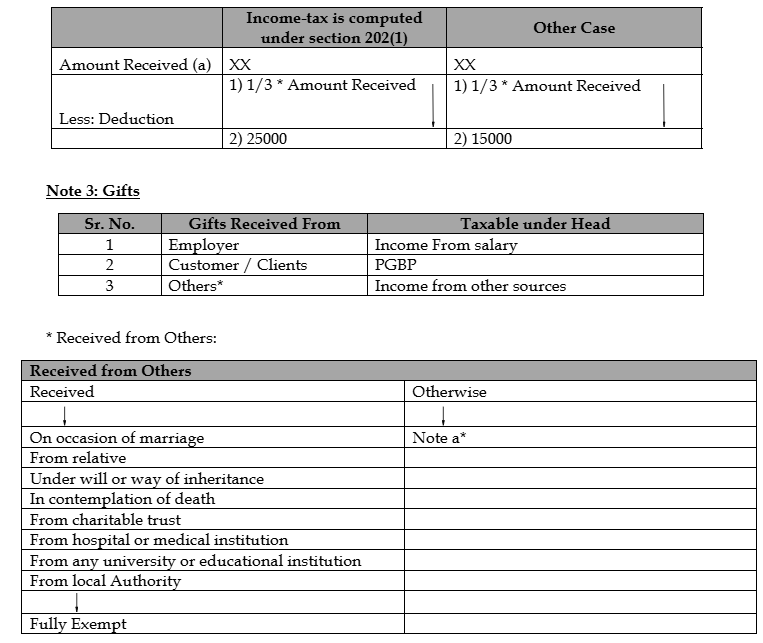

Note 2: Family Pension Received after the death of Employee.

Family Pension is a regular monthly amount payable by the employer to a family member of an employee upon the death of such employee.

Deduction u/s 93(1)(d)(i)

Section 92(2)(j) - Compensation on Termination of employment

Any compensation or other payment, due or received by any person in connection with termination of his employment or modification of its terms and conditions is treated as income u/s 92(2)(j).

The above provision is applicable only when compensation is received from a person other than employer. However, if it is received from employer then it is taxable as profits in lieu of salary under the head income from salary u/s 18(1).

Section 94 – Specific Disallowance

- Personal Expense of the Assessee

- Any Interest paid outside India without deducting TDS.

- Salary paid outside without deducting TDS.

- In case of income from lotteries, crossword puzzles, horse races, card games, gambling, or betting of any kind, no deduction shall be allowed for any related expenditure or allowance. Such income is taxable on a gross basis.

Exception- Horse racing business: The above restriction shall not apply to income earned from the activity of owning and maintaining racehorses. In such cases, relevant expenses may be allowed.

Conclusion:

The comparison between the Income Tax Act, 1961 and the Income Tax Act, 2025 shows that the fundamental concept of “Income from Other Sources” continues to remain largely consistent under both Acts. The new Act mainly focuses on simplifying the language, reorganizing provisions, and improving clarity for better interpretation and compliance. Provisions relating to dividend income, interest income, gifts, winnings, family pension, royalty, and other miscellaneous incomes have been retained with revised section numbering and simplified drafting.

Authors:

Vishal Kothari

Director | LinkedIn Profile

Nitesh Jha

Manager | LinkedIn Profile

Rutwick Ruparelia

Manager

Nidhi Mittal

Associate Consultant | LinkedIn Profile

.svg)