ACQUISITION ACCOUNTING – IND AS 103

Introduction & Meaning of Business Combination

Companies increasingly pursue inorganic growth through mergers and acquisitions. To ensure uniformity in financial reporting, IND AS 103 – Business Combinations (aligned with IFRS 3)governs how such transactions are recorded and reported.

As per IND AS 103, a Business Combination is a transaction or event in which an acquirer obtains control over one or more businesses. A 'business' is an integrated set of activities and assets capable of being conducted for the purpose of providing goods or services or generating income.

The standard mandates the Acquisition Method as the sole method for business combinations. The key steps are:

• Identify the Acquirer

• Determine the Acquisition Date

• Recognise and measure identifiable assets and liabilities at fair value

• Measure the Consideration Transferred

• Measure Non-Controlling Interest (NCI)

• Calculate Goodwill or Bargain Purchase Gain

Under the Companies Act, 2013,business combinations must comply with regulatory requirements including approvals from the National Company Law Tribunal (NCLT) and other statutory bodies.

Why do companies undertake acquisitions?

Companies undertake acquisitions for the following key reasons:

• Synergy Creation: Operational and financial synergies reduce costs and improve capital efficiency, with the combined entity's value exceeding the sum of its parts.

• Market Expansion: Accelerated entry into new geographies or segments, bypassing organic growth timelines.

• Technology& IP Access: Gaining proprietary technology, patents, or skilled talent —particularly in IT and pharma sectors.

• Diversification: Reducing business risk by entering different industries or product lines.

• Enhancing Shareholder Value: Well-executed M&A improves EPS, ROE, and enterprise value.

• Vertical Integration: Acquiring suppliers or distributors to control the supply chain and improve margins.

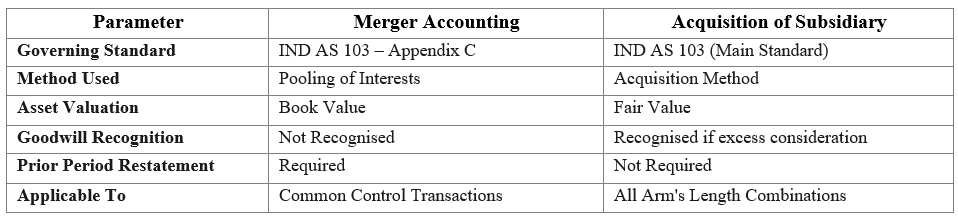

Merger Accounting vs. Acquisition of Subsidiary

Merger Accounting (Pooling of Interests)

Applied when two entities combine as equals with no identifiable acquirer. Assets and liabilities are carried at existing book values, no goodwill is recognised, and prior period financials are restated. Under IND AS 103, this is only permissible for common control transactions.

Acquisition of a Subsidiary (Acquisition Method)

When one entity obtains control over another, IND AS 103 mandates the Acquisition Method. The acquiree's identifiable assets, liabilities, and contingent liabilities are measured at fair value on the acquisition date. Excess consideration over net fair value is recognised as Goodwill, tested annually for impairment under IND AS 36.

Does IND AS 103 Cover Amalgamations?

IND AS 103 specifically excludes business combinations involving entities under common control from its main scope.

• Amalgamations of group companies (e.g., merger of a wholly-owned subsidiary into its parent)are governed by IND AS 103, Appendix C – Business Combinations of Entities Under Common Control, permitting either the Pooling of Interests or the Acquisition Method.

• Amalgamations between unrelated parties (arm's length transactions) must use the Acquisition Method under the main standard.

Note: The older AS 14 recognised both methods for all amalgamations. IND AS 103 eliminates the Pooling of Interests Method for arm's length combinations, aligning India with global IFRS standards.

This article focuses exclusively on the accounting treatment for acquisition of another entity under IND AS 103.The steps and procedures discussed herein pertain solely to such acquisitions.

Regulatory Process for Acquisitions under Companies Act, 2013

Board of Directors Approval

The Board passes a resolution authorising due diligence, appointment of advisors, and exploration of the transaction, satisfying itself that the acquisition serves the company's best interests.

Appointment of Merchant Banker / Valuer

A SEBI-registered Merchant Banker and an independent Registered Valuer are appointed for due diligence, fair value assessment, and transaction structuring. Their valuation report determines the Share Swap Ratio or purchase consideration.

Post-Acquisition Accounting under IND AS 103

Acquisition Date & Record Date

All accounting under IND AS 103 is done as of the Acquisition Date - the date the acquirer obtains effective control. This typically aligns with the date of filing the NCLT order with the ROC or the Record Date for share allotment in a share swap. From this date, all identifiable assets, liabilities, and contingent liabilities of the acquiree are recognised and measured at fair value, and the acquiree's financials are consolidated.

Case Study – Determination of Acquisition Date Based on Transfer of Control

ABC Ltd. (Acquirer) entered into a Share Purchase Agreement and a Share Subscription cum Shareholders' Agreement with XYZ Ltd. (Acquiree) in the financial year 2022-23, pursuant to which shares of XYZ Ltd. were transferred to ABC Ltd. However, despite the transfer of shares, ABC Ltd. did not obtain effective control over XYZ Ltd. at that point in time.

It was only on 20th July 2025 that ABC Ltd. obtained effective control over XYZ Ltd., and accordingly, this date is recognised as the Acquisition Date under IND AS 103. As per IND AS 110,control requires the acquirer to have power over the investee, exposure or rights to variable returns from its involvement with the investee, and the ability to use that power to affect those returns. Since all three conditions were met only on 20th July 2025, the mere transfer of shares in 2022-23 did not trigger acquisition accounting.

Consequently, all accounting under IND AS 103 including recognition and fair value measurement of identifiable assets and liabilities assumed, computation of goodwill, and recognition of non-controlling interest is carried out as of 20th July 2025, being the date on which control effectively passed to ABC Ltd.

Key Accounting Steps

• Recognition of Assets & Liabilities: Identifiable assets (including previously unrecorded intangibles such as customer relationships, brand names, patents)and liabilities are recorded at fair value on the acquisition date.

• Consideration Transferred: Includes cash paid, fair value of shares issued, contingent consideration (earn-outs), and any previously held equity interest remeasured at fair value.

• Goodwill: Goodwill = Consideration Transferred + NCI + Fair Value of Previously Held Interest - Net Fair Value of Identifiable Assets and Liabilities. Goodwill is not a mortised; it is tested annually for impairment under IND AS 36.

• Bargain Purchase (Negative Goodwill): If net fair value of assets acquired exceeds the consideration, the difference is recognised as a gain in the Statement of Profit and Loss, after reassessment.

• Measurement Period: Up to one year from the acquisition date to retrospectively adjust provisional fair values as additional information becomes available.

• Non-Controlling Interest (NCI): Measured either at proportionate share of net identifiable assets or at full fair value (full goodwill method), as an accounting policy choice.

Case Scenarios for Goodwill Computation

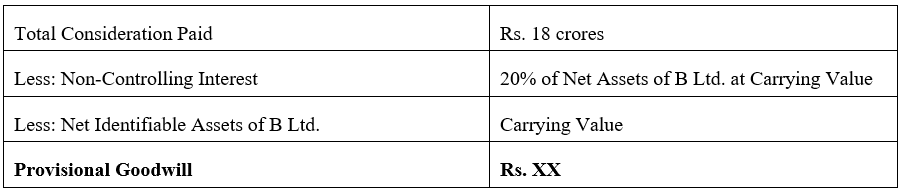

1. Provisional Goodwill Recognition and Purchase Price Allocation Report

A Ltd., a listed company, acquired an 80% stake in B Ltd. on1st July 2025 by investing a total consideration of INR 18 crores. In accordance with IND AS 103, acquisition accounting was required to be performed as of 1st July 2025, being the Acquisition Date on which control over B Ltd. was obtained by A Ltd.

Provisional Accounting at the Date of Acquisition (Quarter Ended 30th September,2025)

As mandated under IND AS 103, the identifiable assets acquired and liabilities assumed of B Ltd. were required to be recognised and measured at their fair values as on the Acquisition Date. However, a Fair Valuation Report from a Registered Valuer could not be obtained within the requisite timeframe for the purpose of preparing the quarterly financial statements.

In view of this, A Ltd. exercised the option available under the Measurement Period provisions of IND AS 103, whereby provisional values maybe used if the initial accounting for a business combination is incomplete at the end of the reporting period. Accordingly, the assets and liabilities of B Ltd. were recorded at their carrying values as on 1st July 2025. Goodwill was provisionally computed as follows:

This provisional goodwill was recognised in the consolidated balance sheet of A Ltd. as on 30th September 2025.

Purchase Price Allocation (PPA) Report – Year End Finalisation

For the purpose of the year-end statutory audit for the financial year ending 31st March 2026, A Ltd. obtained a Purchase Price Allocation (PPA) Report from a Registered Valuer in accordance with the requirements of IND AS 103. The PPA Report assessed the fair values of all identifiable assets and liabilities of B Ltd. as on the Acquisition Date.

Upon completion of the fair valuation exercise, it was determined that none of the assets or liabilities of B Ltd. required a fair value adjustment, as there were no assets in the books of B Ltd. whose fair value differed materially from their carrying value. Consequently, the carrying values were confirmed as a reasonable approximation of fair values.

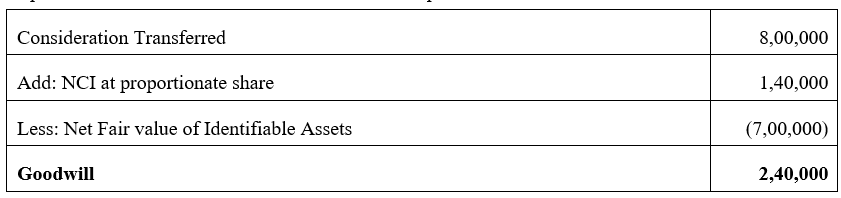

2. Secondary Purchase of Shares

A Ltd. (Acquirer) purchases 80% of the equity shares of B Ltd. (Acquiree) from its existing shareholders for Rs. 8,00,000. On the acquisition date, the fair value of B Ltd.'s net identifiable assets is Rs. 7,00,000.

Impact: Since no new shares are issued and no cash flows into the acquiree, the acquiree's net assets, share capital, and reserves remain exactly as they were before the transaction. Only the ownership of the existing shares changes hands.

NCI is measured at its proportionate share = 20% × 7,00,000 = 1,40,000

Goodwill computation: -

Goodwill is the excess of the price paid by the acquirer over the acquirer's share of the net fair value of the acquiree's identifiable assets and liabilities on the acquisition date.

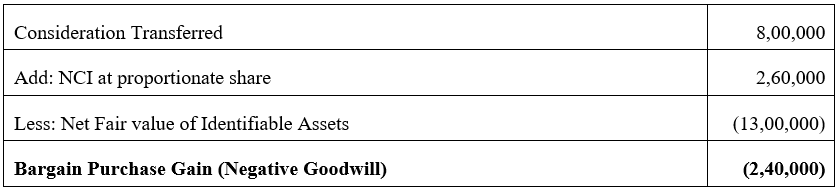

3. Fresh Issue of Shares

A Ltd. (Acquirer) subscribes to fresh shares issued by B Ltd. (Acquiree), paying Rs.8,00,000 for an 80% stake. The cash flows directly into B Ltd.

Before the fresh issue, the fair value of B Ltd.'s net identifiable assets was Rs. 5,00,000.

After the fresh issue, B Ltd.'s net assets increase by Rs. 8,00,000 making the total net identifiable assets Rs. 13,00,000.

Impact: Unlike a secondary purchase, a fresh issue increases the acquiree's net assets because the consideration paid by the acquirer flows directly into the acquiree as cash or other assets. The share capital and share premium of the acquiree increase by the amount of the fresh issue.

· Share Capital of the Acquiree increases by the face value of shares issued.

· Securities Premium increases by the excess of issue price over face value.

· Cash / Bank of the Acquiree increases by the total consideration received.

NCI(20%) = 20% of INR 13,00,000 = Rs. 2,60,000

Goodwill computation: -

Since the acquiree's net assets increase by the amount of consideration received, the net fair value of identifiable assets is higher compared to a secondary purchase. Goodwill therefore reflects the premium paid over and above the enhanced post-issue net asset value attributable to the acquirer.

Conclusion

IND AS 103 provides a robust, globally aligned framework ensuring that acquisitions are reported at economic reality through the Acquisition Method. The Companies Act, 2013 complements this with a structured regulatory approval process safeguarding the interests of all stakeholders. Companies embarking on acquisitions must ensure meticulous compliance with both the accounting standards and the regulatory framework to achieve a seamless and value-accretive transaction.

.svg)