INTERMEDIARY SERVICES UNDER GST

A STRUCTURAL SHIFT TOWARDS EXPORT RECOGNITION

For several years, Indian businesses engaged in liaison, facilitation, brokerage, sourcing support, and backend coordination services for overseas clients faced prolonged GST disputes regarding the taxability of intermediary services. Although these services were rendered to foreign customers and consideration was received in foreign exchange, the transactions were frequently denied export status due toa special place-of-supply provision under the Integrated Goods and Services TaxAct, 2017 (“IGST Act”).

The Finance Act, 2026 has now introduced a major legislative correction by omitting Section13(8)(b) of the IGST Act with effect from 30 March 2026. As a result, intermediary services supplied to overseas recipients will now generally be governed by the default place-of-supply rule under Section 13(2), thereby enabling such transactions to qualify as exports of services, subject to fulfillment of prescribed conditions.

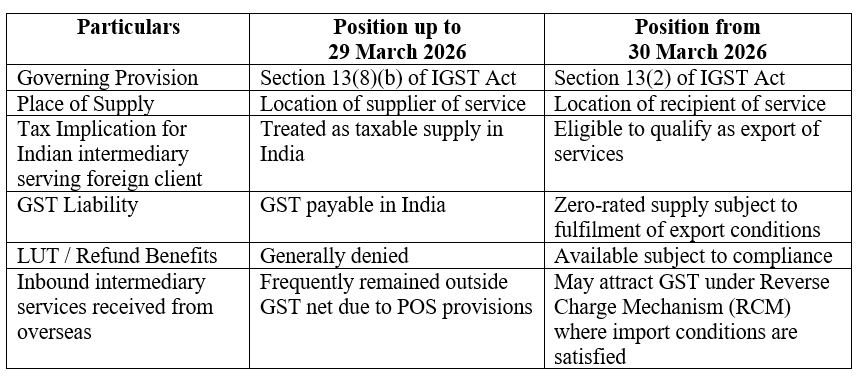

1. Legal Position: Before and After30 March 2026

The dispute primarily originated from Section 13(8)(b) of the IGST Act, which earlier prescribed a special place-of-supply rule for intermediary services.

The omission of Section 13(8)(b) aligns intermediary services with the broader destination-based taxation principle forming the foundation of the GST regime.

2. Meaning of “Intermediary” Under GST

Before claiming export benefits, businesses must first evaluate whether their activities actually qualify as “intermediary services” under Section 2(13) of the IGST Act.

As per the statutory definition, an intermediary generally refers to a broker, agent, or any person who arranges or facilitates the supply of goods or services between two or more parties, but does not include a person supplying such goods or services on their own account.

CBIC Circular No. 159/15/2021-GST dated 20 September 2021 clarified certain guiding principles for determining intermediary status.

Broad Indicators of Intermediary Arrangement

1. Presence of Three Parties

The transaction normally involves:

- Two principal parties involved in the main supply; and

- One facilitating party arranging or facilitating such supply.

2. Facilitation Role

The intermediary acts in the nature of a broker, commission agent, coordinator, sourcing agent, or facilitator for the principal supply.

3. No Supply on Own Account

If the Indian entity independently provides the main service on a principal-to-principal basis, it generally would not qualify as an intermediary.

For example:

- Software development services,

- Data hosting services,

- Independent consultancy,

- Customer support services performed on own account,

- Market research or technical support services,

provided directly to overseas clients may continue to qualify as regular export services and may not fall within intermediary classification.

3. Conditions for Export of Intermediary Services

Even after the legislative amendment, intermediary services will qualify as exports only when all conditions prescribed under Section 2(6) of the IGST Act are satisfied.

The following conditions remain critical

- The supplier of service must be located in India.

- The recipient of service must be located outside India.

- The place of supply must be outside India.

- Payment must be received in convertible foreign exchange or in Indian Rupees wherever permitted under RBI regulations.

- Supplier and recipient should not merely be establishments of the same legal person.

Once these conditions are satisfied, intermediary services supplied to overseas clients may qualify as zero-rated exports eligible for:

- Supply under Letter of Undertaking (LUT) without payment of IGST;

- Refund of unutilised Input Tax Credit (ITC);

- Export-related GST benefits available under the IGST framework.

4. Impact on Import of Intermediary Services and RCM Exposure

While the amendment provides substantial relief for Indian exporters of intermediary services, it may simultaneously increase GST implications for Indian businesses receiving intermediary services from foreign entities.

Under the earlier regime, overseas commission agents or foreign intermediaries often remained outside the GST net because the place of supply was deemed to be the location of the supplier situated outside India.

Post omission of Section 13(8)(b), intermediary services may now be governed by the general place-of-supply provision under Section 13(2), meaning the place of supply would ordinarily shift to the location of the Indian recipient.

Consequently, where the conditions of “import of services” are satisfied, Indian businesses engaging foreign brokers, sourcing agents, or overseas commission agents may be required to discharge GST under Reverse Charge Mechanism (RCM), subject to applicable exemptions and notifications.

Businesses dealing with overseas agents should therefore re-evaluate:

- Existing agreements;

- GST implications on commission structures;

- RCM applicability;

- ITC eligibility;

- Contractual tax clauses.

5. Transitional Considerations and Time of Supply

The Finance Act, 2026 does not contain a dedicated transitional saving provision specifically dealing with intermediary services. Accordingly, taxability may largely depend upon the applicable time-of-supply provisions under the GST law.

Businesses should therefore carefully examine:

- Date of invoice;

- Date of payment or advance receipt;

- Date of completion of service;

- Nature of continuous supply contracts.

Broad Practical Understanding

1. Transactions Prior to 30 March 2026

Invoices or supplies falling under the pre-amendment regime may continue to be governed by the earlier provisions applicable during that period.

2. Advances Received Before 30 March 2026

Tax treatment may require evaluation based on applicable time-of-supply provisions and contractual terms.

3. Supplies Made From 30 March 2026 Onwards

Cross-border intermediary services supplied to overseas recipients may qualify as exports subject to fulfillment of export conditions and proper LUT compliance.

Given the absence of specific transition provisions, businesses should maintain proper documentation supporting the timing of supply and tax position adopted.

6. Key Takeaways

The omission of Section 13(8)(b) represents a significant policy shift in India’s GST framework. The amendment aligns intermediary taxation with the destination-based philosophy underlying GST and removes a long-standing anomaly that resulted in extensive litigation.

For Indian businesses servicing overseas clients, the amendment may substantially improve:

- Global competitiveness;

- Working capital efficiency;

- Refund eligibility;

- Export-oriented business structuring.

At the same time, Indian recipients procuring intermediary services from overseas entities should proactively evaluate potential reverse charge exposure arising from the revised place-of-supply framework.

Considering the historical litigation surrounding intermediary classification itself, businesses should continue to examine contractual arrangements carefully to determine whether their services genuinely qualify as intermediary services or constitute independent principal-to-principal supplies.

Authors:

CA Jalpesh Vora | Partner

Bhavik Shah | Manager

.svg)