India's New Labour Codes: Key Changes and Audit Considerations

Executive summary

India has replaced twenty-nine central labour laws with four consolidated Codes, and the new regime is now live. The single change with the widest reach is a uniform definition of wages that, in effect, requires basic pay and dearness allowance to make up at least half of an employee's total remuneration. That one change flows through to provident fund, gratuity, bonus, leave encashment and the employee state insurance contribution, raising both cost and provisioning for many employers. Alongside it sit new rules on fixed-term employment, contract labour, working hours, social security for gig workers and a digitised, portal-based compliance architecture. For internal audit the task is twofold: to test the financial and payroll impact of the wage definition, and to check that the organisation's compliance, documentation and provisioning keep pace with the new framework during a transition in which several State Rules are still being finalised.

The reform in brief: four Codes in place of twenty-nine laws

On 21 November 2025 the Ministry of Labour and Employment brought all four Labour Codes into force through notifications in the Official Gazette, supported by a press release and a corrigendum issued on 19 December 2025. The four are the Code on Wages, 2019, the Industrial Relations Code, 2020, the Code on Social Security, 2020 and the Occupational Safety, Health and Working Conditions Code, 2020. Together they consolidate and replace twenty-nine central labour statutes.

The operational detail comes from the rules made under the Codes. The Ministry published draft Central Rules on 30 December 2025 and notified the final Central Rules on 8 May 2026: the Code on Wages (Central) Rules, 2026, the Social Security (Central) Rules, 2026, the Industrial Relations (Central)Rules, 2026 and the Occupational Safety, Health and Working Conditions(Central) Rules, 2026. Because labour is a concurrent subject, the Central Rules apply where the Central Government is the appropriate government, covering sectors such as banking, insurance, telecommunications, mines, major ports, air transport and central public sector undertakings, while each State must notify its own rules for establishments under its jurisdiction. Several States have done so and many are still at the draft stage. The Ministry has also issued FAQs, most recently on 16 March 2026, which give useful administrative guidance, although the Ministry itself states that the FAQs are not legally binding and that the text of the Codes prevails in any conflict.

The changes that matter for audit

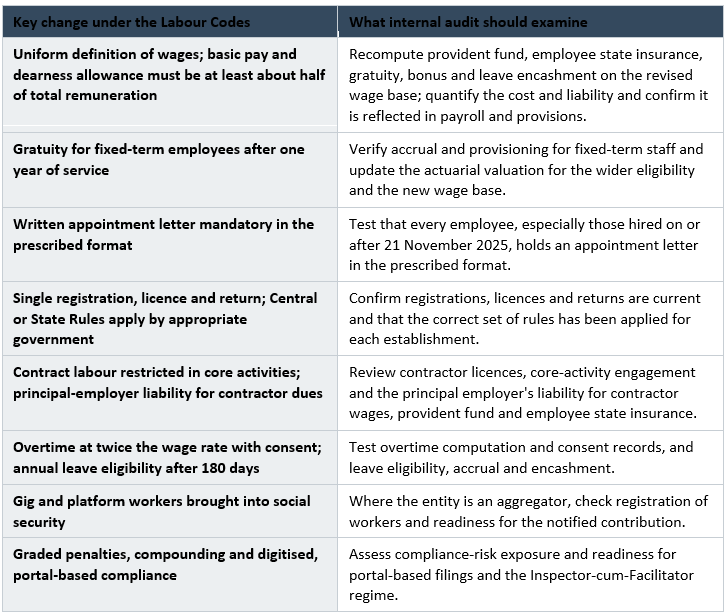

The new definition of wages

The most consequential change is the uniform definition of wages that now runs through all four Codes. Wages comprise basic pay, dearness allowance and any retaining allowance, and exclude a specified list of components such as house rent allowance, conveyance, overtime, bonus, commission and the employer's contribution to provident fund. The Codes add a crucial proviso: if the excluded components together exceed one-half of total remuneration, the excess is added back to wages. The practical effect is that basic pay and dearness allowance must amount to at least about half of total remuneration. Since provident fund, gratuity, bonus, leave encashment and the employee state insurance contribution are all computed on wages, employers whose pay structures carry a low basic and large allowances will see these costs and liabilities rise. The Ministry's FAQs confirm that the revised definition governs these computations with effect from 21 November 2025.

Social security: gratuity, provident fund and gig workers

Under the Code on Social Security, fixed-term employees become eligible for gratuity after one year of continuous service, rather than the five years that continue to apply to other employees except in cases of death or disablement. The existing gratuity ceiling continues until the Government modifies it, and gratuity is computed on the new wages base. Provident fund and the employee state insurance contribution are likewise computed on the new definition, although, pending finalisation of certain limits, thresholds such as the existing wage ceiling for employee state insurance coverage continue to apply, as the FAQs clarify. The Code also brings gig and platform workers within the social security net: aggregators are required to register such workers on the designated portal and to contribute to a dedicated social security fund at a rate and in a manner to be notified by the Central Government.

Employment terms: fixed-term staff, contract labour and appointment letters

Fixed-term employment now has statutory recognition, and fixed-term employees are entitled to the same wages and benefits as permanent staff doing similar work. The engagement of contract labour is restricted, with applicability set at fifty workers and limits on the use of contract labour in core activities, and with continuing obligations on the principal employer for the wages and social security of contract workers. The Occupational Safety, Health and Working Conditions Code makes a written appointment letter mandatory for every employee, and the rules prescribe its format, which is a simple but significant documentation requirement.

Working hours, overtime and leave

Working hours are standardised, overtime is payable at twice the normal rate of wages and requires the worker's consent, and the FAQs clarify that overtime is computed from the eighth hour even where a longer maximum working day is permitted. Eligibility for annual leave with wages now arises after one hundred and eighty days of work in a year, a lower threshold than under the earlier law.

Industrial relations and the compliance architecture

The Industrial Relations Code raises the threshold for standing orders and for prior permission for lay-off, retrenchment and closure to three hundred workers, provides for a worker re-skilling fund to which the employer contributes on retrenchment, and sets out the recognition of negotiating unions. Across the Codes, compliance is being simplified and digitised through a single registration, a single licence and a single return, web-based filings, and an Inspector-cum-Facilitator who both advises and enforces. Penalties a regraded, many offences can be compounded, and in some cases there is an opportunity to comply before prosecution.

A summary view: change and audit focus

What internal audit should focus on

Translating the new regime into an audit programme means looking across payroll, financial reporting, statutory compliance and documentation. The main areas of coverage are set out below.

Payroll and the wage definition

· Whether basic pay plus dearness allowance, and any retaining allowance, meets at least half of total remuneration for each employee, and whether excluded allowances above that limit have been added back to wages.

· Whether provident fund, employee state insurance, gratuity, bonus and leave encashment have been recomputed on the revised wage base, and the additional cost quantified.

· Whether any restructuring of cost-to-company keeps take-home pay and benefits within the law and does not breach minimum or floor wages.

Provisioning and financial reporting

· Whether the gratuity actuarial valuation under AS 15 or Ind AS 19 reflects the new wage base and the one-year eligibility for fixed-term employees, and whether the provision is adequate.

· Whether provisions for leave encashment and bonus, and the higher employer cost of provident fund and employee state insurance, are recognised, and whether disclosures and any contingent liabilities are appropriate.

Statutory compliance and documentation

· Whether statutory dues are computed on the correct base, deposited within due dates and reconciled to the returns filed.

· Whether appointment letters, electronic wage slips, registers and muster rolls follow the prescribed formats, and whether registrations, licences and returns are current.

Contractlabour and fixed-term employment

· Whether fixed-term employees receive wages and benefits on par with permanent staff and gratuity is provided after one year of service.

· Whether contract labour is engaged within the permitted limits and not in core activities, and whether the principal employer's obligations for contractor dues are met.

Transition and change management

· Whether the entity has mapped which provisions are in force, which await State Rules, and the basis on which it is complying in the meantime.

· Whether HR, payroll, finance and legal have aligned, payroll systems have been updated for the new wage definition, and the entity is ready for portal-based filings and inspections.

The transition and dual-compliance risk

The transition deserves particular attention. The Codes are in force and the Central Rules are notified, but many State Rules are still being finalised, and certain limits and thresholds continue to apply until the Government modifies them. Existing rules and notifications under the repealed laws continue to operate where they do not conflict with the Codes. The Ministry's FAQs are helpful but, as noted, non-binding. For internal audit this means confirming that the organisation has mapped which provisions are in force, which await State Rules, and the basis on which it is complying in the meantime, and that compliance positions are documented and revisited as further notifications appear. SA 250 of the Standards on Auditing, on the consideration of laws and regulations in an audit, and SA 540, on auditing accounting estimates, are useful anchors for the auditor's approach to both compliance and the related provisions.

Conclusion

The Labour Codes are the most significant change to India's employment-law landscape in decades, and they are no longer a future event: they are in force, with the Central Rules notified and State Rules following. Their effect is felt most immediately in payroll and in the provisions that depend on the definition of wages, but it reaches documentation, contract labour, social security and the way compliance itself is administered. Internal audit adds the most value by testing the financial and payroll impact rigorously, by checking that compliance and documentation keep pace, and by giving management and the Audit Committee an early and clear view of exposure while the regime settles. Acting during the transition, rather than waiting for the first inspection, is the surest way to manage both cost and risk.

.svg)