What are the different aspects of valuation, the company needs to consider at the time of issue/ transfer of shares?

With the boom in Startups, we are witnessing many corporate events like fund-raise, secondary sale of securities, ESOPs, etc. With these transactions, the aspect of valuation has become more prominent now than ever. There are various regulations under the Income Tax Act, 1961, Companies Act 2013, and FEMA 1999 which regulate the valuation of securities.

The Companies, Investors as well as all the stakeholders should exercise utmost caution while closing any primary or secondary share transactions.

In this article, we have explained different aspects to be considered by Start-ups, Founders, and Investors while pursuing such transactions:

A.ISSUE OF SHARES:

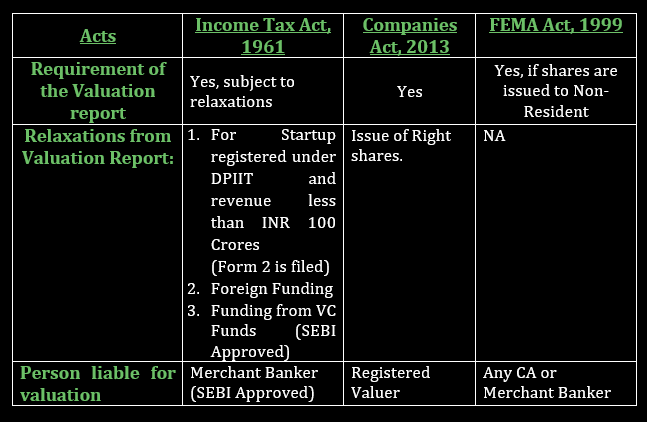

Valuation aspects to be considered when Company is raising funds through private placement:

B. Transfer of Shares:

Valuation aspects to be considered during the secondary sale of shares:

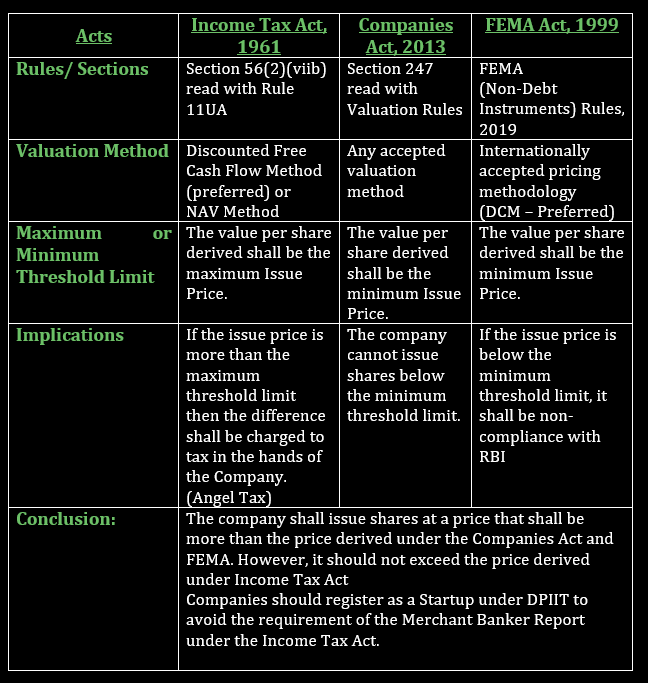

- As per Section 56(2)(x) of Income Tax Act 1961, in case any shares or securities are transferred at a value that is less than the Fair Market Value, the difference shall be charged to tax in the hands of the buyer.

- Fair market value under the Income Tax Act for the purpose of secondary sales of shares shall be computed in the following ways:

- In the case of a listed company, it shall be listed price

- In the case of an unlisted company, it shall be computed using the formula prescribed under Rule 11UA (i.e., Book Value)

- There are no related provisions on the Valuation of shares under the Companies Act with respect to the transfer of Shares

- As per FEMA Regulations (Non-Debt Rules, 2019), when shares are transferred from a Non-Resident to Resident or vis-à-vis, the transaction price shall be greater than the value derived by CA or merchant banker using an internationally accepted methodology.

When ESOPs are exercised, the Perquisite value shall be taxable in the hands of employees under section 49(2AA) read with section 17(2) of Income Tax Act, 1961.

Perquisite value shall be calculated as the difference between Fair Market Value and the amount actually paid (exercised price).

Fair market value under the Income Tax Act for the purpose of ESOPs shall be computed in the following ways:

- In the case of a listed company, it shall average of opening and closing price on the date of allotment.

- In the case of an unlisted company, value is determined by Merchant Banker. There is no such relaxation provided to the Startups in case of exercising of ESOPs.

(In case you want to know more about Issue or Transfer of share, shall connect over following mails)

CA Shreyans Dedhia

Partner | Email: shreyans.dedhia@masd.co.in

Kiwa Shah

Associate Consultant | Email: kiwa.shah@masd.co.in

.svg)